Need money immediately for business or any other reason? Taking a loan against property can help you meet your funding requirement if you haven’t got enough savings to meet some unexpected need.

What is Loan Against Property?

As the name suggests, a loan taken from a lender with your property as a collateral is called loan against property or LAP. You can take a loan against your house, apartment, office, showroom, shop or land as a collateral or security. A loan against property is a secured loan because the lender can sell the property to get its money back from the borrower in case of a default.

- Interest Rates: 12-16% per annum

- Property Type: Both residential and commercial properties accepted as collateral

- Flexible Product Offerings: EMI-based loans or an overdraft facility for a more flexible loan

- Easy Repayments: Longer repayment tenure & EMI is lower than other funding options

- Loan Amount to Property Value: 40-75% of the property value

The lender will offer you a loan depending upon the value of the property as well as your repayment capacity. Many people incorrectly think that the loan eligibility amount for a loan against property solely depends on the value of the property. Generally, banks conduct their due diligence for the property concerned, and offer up to 75% of its market value as loan. The tenure of a loan against property is 1-10 years, but some banks offer loans for longer tenures as well. The interest rate for a loan against property, which can be floating interest rate or fixed interest rate, varies from 12-16%, which makes them cheaper than personal loans (see table).

Being a secured loan, you can get a higher loan amount when taking a loan against property in comparison with an unsecured loan such as a personal loan.

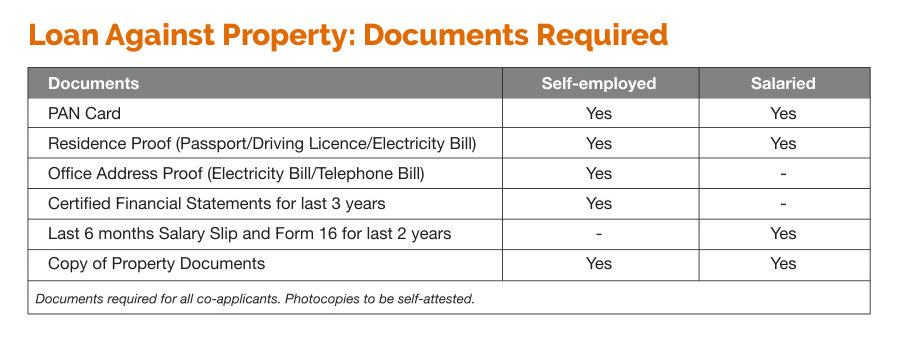

Eligibility & Documents Required for Loan Against Property

Whether you need money to expand your business or fund your personal requirements, you can get a loan against property if you meet the eligibility criteria according to your employment status.

If you are a salaried individual, the process is relatively simpler. You will require your proof of identity and residence, latest bank statement showing your salary/income being credited for the past 6 months, salary slip for last six months, tax returns for last 2-3 years, and copies of all property documents of the property concerned against which you need a loan.

If you are a self employed professional/individual, you will have to submit your identity and address proof, certified financial statement for the last 3 years, latest bank statement showing your income being credited from the past 6 months, and copies of all documents of the property that you want to pledge for the loan.

Age Limit: Banks require that the borrower has a source of income/employment until the loan is paid off. For loan against property, the maximum age of a borrower at the end of the loan tenure cannot exceed 60 years for salaried individuals (retirement age in India) and 70 years for self-employed individuals.

How to Get a Loan Against Property

First, check if you are eligible for a loan with adequate repayment capacity as your salary or income. The property to be mortgaged must have clear title. If the property you intend to pledge for the loan has multiple owners, you will have to apply for a loan with all of them as joint applicants. You can get a loan against any property, and it can also be let out on rent.

The bank will require all the documents related to the property, and also require your identity and address proof. In addition, you will have to furnish your bank statements and income proof as applicable based on whether you are salaried or self-employed.

Your credit score will also be analysed before sanction of your loan against property application. Any payment default such as non-payment of credit card bills, will lower your chances of getting a loan. Once the bank is satisfied with the property ownership and your creditworthiness, it will sanction a loan, which will be the lower of the two: your loan amount eligibility based on your repayment capacity or 40-75% of the property value.